How Personal Financial Statements Help Track Financial Progress

- rhpersonalbookkeep

- May 19

- 6 min read

Managing personal finances involves more than simply paying bills and monitoring a bank account balance. Understanding overall financial health requires organization, planning, and accurate financial tracking. One of the most effective ways to monitor financial progress is through personal financial statements.

Personal financial statements provide a structured overview of income, expenses, assets, liabilities, and net worth. These statements help individuals evaluate spending habits, identify financial strengths and weaknesses, and make informed decisions regarding budgeting, saving, debt reduction, and long-term goals.

Many people only review their finances when facing financial stress or preparing for taxes. However, regularly maintaining personal financial statements can help individuals stay proactive instead of reactive. Organized financial records create a better understanding of where money is going and how financial decisions affect long-term stability.

Whether someone is working toward paying off debt, saving for a home, preparing for retirement, or building investments, personal financial statements serve as valuable tools for measuring financial progress over time.

WHAT ARE PERSONAL FINANCIAL STATEMENTS?

Personal financial statements are documents that summarize an individual’s financial position and financial activity. These statements help organize financial information into categories that are easier to understand and analyze.

The two primary personal financial statements include:

Personal Balance Sheet (Statement of Net Worth)

Personal Income Statement (Cash Flow Statement)

Together, these statements provide a complete picture of someone’s financial condition.

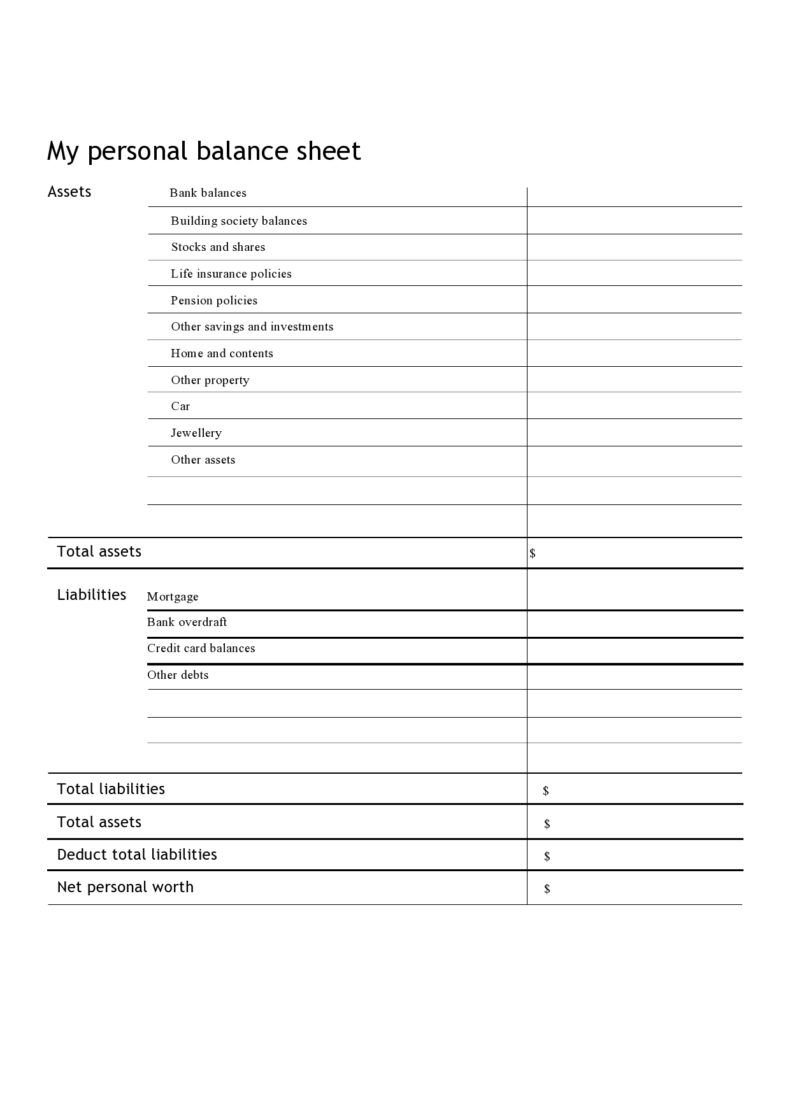

THE PERSONAL BALANCE SHEET

The personal balance sheet measures financial position at a specific point in time. It shows what someone owns and what someone owes.

The formula is:

Assets - Liabilities = Net WorthAssets

Assets are items with financial value. Common personal assets include:

Cash

Checking accounts

Savings accounts

Retirement accounts

Investments

Vehicles

Real estate

Personal property

Assets are usually categorized as either current assets or long-term assets.

Current Assets

Current assets are liquid or easily converted into cash, such as:

Cash

Savings

Emergency funds

Long-Term Assets

Long-term assets may include:

Homes

Vehicles

Retirement investments

Brokerage accounts

Liabilities

Liabilities represent debts or financial obligations.

Examples include:

Mortgages

Credit card balances

Auto loans

Student loans

Personal loans

Tracking liabilities is important because debt impacts cash flow, savings potential, and overall financial flexibility.

Net Worth

Net worth is one of the most important measurements of financial progress.

A positive net worth means assets exceed liabilities. A negative net worth means debts are greater than assets.

Monitoring net worth over time helps individuals:

Measure financial improvement

Track debt reduction

Evaluate savings growth

Stay motivated toward long-term goals

THE PERSONAL INCOME STATEMENT

The personal income statement focuses on cash flow over a period of time, usually monthly.

This statement tracks:

Income

Expenses

Savings

Remaining cash flow

The formula is:

Income - Expenses = Net Cash FlowIncome Categories

Income may include:

Employment income

Self-employment income

VA benefits

Retirement income

Dividend income

Side business income

Tracking all income sources provides a realistic understanding of total monthly cash flow.

Expense Categories

Expenses are commonly divided into categories such as:

Needs

Housing

Utilities

Groceries

Insurance

Transportation

Wants

Entertainment

Dining out

Subscriptions

Shopping

Savings and Investments

Emergency savings

Retirement contributions

Investment accounts

Organizing expenses into categories helps identify spending patterns and opportunities for improvement.

HOW PERSONAL FINANCIAL STATEMENTS HELP TRACK FINANCIAL PROGRESS

Want help organizing your personal finances and tracking financial progress?

1. Improving Financial Awareness

Many people underestimate how much they spend or overlook recurring expenses. Financial statements provide clarity by organizing financial activity into measurable categories.

This increased awareness can help:

Reduce overspending

Improve budgeting

Identify unnecessary expenses

Create better financial habits

2. Measuring Net Worth Growth

Net worth is one of the clearest indicators of financial progress.

As debts decrease and assets grow, net worth improves over time. Even small monthly improvements can create significant long-term financial growth through consistency and compounding.

3. Supporting Better Budgeting

Personal financial statements make budgeting more accurate and realistic.

Instead of guessing where money goes each month, individuals can review actual spending patterns and make informed adjustments.

Budgeting becomes more effective when supported by:

Organized expense tracking

Income monitoring

Debt analysis

Savings goals

4. Identifying Debt Problems Early

Debt can become difficult to manage when balances grow faster than income.

Financial statements help individuals:

Track debt balances

Monitor payment progress

Compare debt to income

Prioritize repayment strategies

Identifying financial issues early allows people to make adjustments before problems become more severe.

5. Encouraging Savings and Investing

Tracking financial progress often motivates individuals to save and invest more consistently.

As savings balances and investment accounts grow, financial statements provide visible proof of progress. This can help reinforce long-term financial discipline.

THE IMPORTANCE OF CONSISTENCY

Financial statements are most effective when updated consistently.

Monthly reviews help individuals:

Track spending

Adjust budgets

Monitor debt

Measure savings progress

Prepare for future expenses

Consistency creates accountability and improves long-term financial decision-making.

COMMON MISTAKES PEOPLE MAKE

Some common financial tracking mistakes include:

Ignoring small recurring expenses

Failing to track debt balances

Not reviewing statements regularly

Mixing personal and business expenses

Relying only on bank balances

Financial statements provide a more complete picture than simply checking a bank account balance.

HOW TECHNOLOGY HELPS PERSONAL FINANCIAL TRACKING

Modern financial tracking tools can simplify organization and reporting.

Many individuals use:

Google Sheets

Excel spreadsheets

Budgeting apps

Accounting software

Spreadsheets remain popular because they provide:

Flexibility

Customization

Detailed reporting

Manual control over categories and calculations

HOW PERSONAL FINANCIAL STATEMENTS SUPPORT LONG-TERM GOALS

Financial statements support goals such as:

Paying off debt

Buying a home

Building emergency savings

Retirement planning

Investment growth

Starting a business

Without organized financial records, long-term planning becomes much more difficult.

CONCLUSION

Personal financial statements are valuable tools for improving financial organization, awareness, and long-term planning. By tracking assets, liabilities, income, expenses, and net worth, individuals gain a clearer understanding of their overall financial health.

Financial progress rarely happens overnight. However, consistent financial tracking can help individuals make informed decisions, reduce financial stress, and stay focused on achieving long-term goals.

Whether someone is beginning a budgeting journey or working toward advanced financial planning, personal financial statements provide a foundation for better financial decision-making and long-term financial stability.

Frequently Asked Questions (FAQs)

What is a personal financial statement?

A personal financial statement is a document that summarizes an individual’s financial position. It typically includes assets, liabilities, income, expenses, and net worth. These statements help track financial progress and improve financial decision-making.

Why are personal financial statements important?

Personal financial statements help individuals:

Track income and expenses

Monitor debt balances

Measure net worth growth

Improve budgeting

Prepare for long-term financial goals

They provide a clearer understanding of overall financial health.

How often should personal financial statements be updated?

Most people benefit from updating their personal financial statements monthly. Regular updates help track spending patterns, monitor savings progress, and identify financial issues early.

What is included on a personal balance sheet?

A personal balance sheet includes:

Assets (cash, savings, investments, property)

Liabilities (loans, credit cards, mortgages)

Net worth

The formula used is:

Assets - Liabilities = Net WorthWhat is a personal income statement?

A personal income statement tracks money flowing in and out over a period of time, usually monthly. It includes:

Income sources

Expenses

Savings

Remaining cash flow

This statement helps individuals understand spending habits and budgeting needs.

Can Google Sheets or Excel be used for personal financial statements?

Yes. Many individuals use Google Sheets or Excel to create personal financial statements because they provide flexibility, customization, and detailed tracking capabilities.

How do personal financial statements help with budgeting?

Personal financial statements organize financial activity into categories, making it easier to:

Identify unnecessary spending

Create realistic budgets

Monitor financial goals

Improve overall financial awareness

What is net worth?

Net worth represents the difference between total assets and total liabilities. It is one of the most important measurements of financial progress.

A positive net worth means assets exceed debts, while a negative net worth means liabilities are greater than assets.

Do personal financial statements help reduce financial stress?

Organized financial tracking can help reduce financial stress by improving awareness and helping individuals feel more in control of their finances. Reviewing financial information regularly allows for better planning and decision-making.

Are personal financial statements useful for long-term financial planning?

Yes. Personal financial statements help support long-term goals such as:

Paying off debt

Building emergency savings

Investing

Retirement planning

Purchasing a home

Starting a business

Tracking financial progress consistently helps individuals stay focused on long-term financial stability.

Learn how organized budgeting and personal financial tracking can help improve financial awareness and long-term financial stability.

Comments